Wall Street spent the last year obsessing over AI earnings calls and GPU shipments. But while the market got caught up with shiny new tech, something far less fashionable was moving, with big implications.

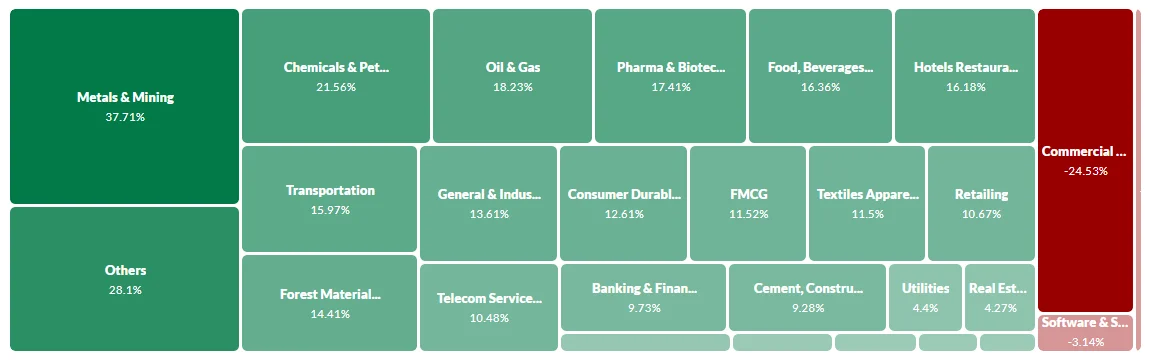

For most of the last decade, mining was the market’s underperformer, capital-intensive, politically risky, and prone to value destruction. It's now got its makeover. Metals and mining have emerged as one of the best-performing segments this quarter, and the move is not driven by a short-term rebound in prices. Tech companies that used to be asset-light are leaning heavily into building physical infrastructure, as data center capex soars. This is driving demand for key metals higher.

Jeff Currie, Chief Strategy Officer at Carlyle, said, “Anything that has an atomic number to it is going up right now. What’s going on in the metals space is hoarding, driven by the 'Three Ds': Debasement, De-dollarization, and Defense.”

“Mining stocks have moved from a boring defensive to an essential portfolio piece. It is one of the few sectors positioned to capture both shifting monetary policy dynamics and an increasingly volatile geopolitical landscape,” said Dilin Wu, a research strategist at Pepperstone Group in Melbourne.

Geopolitical shift: China forces a rethink

Geopolitics is causing volatility across markets, with rising export controls, tariffs, and strategic stockpiling.

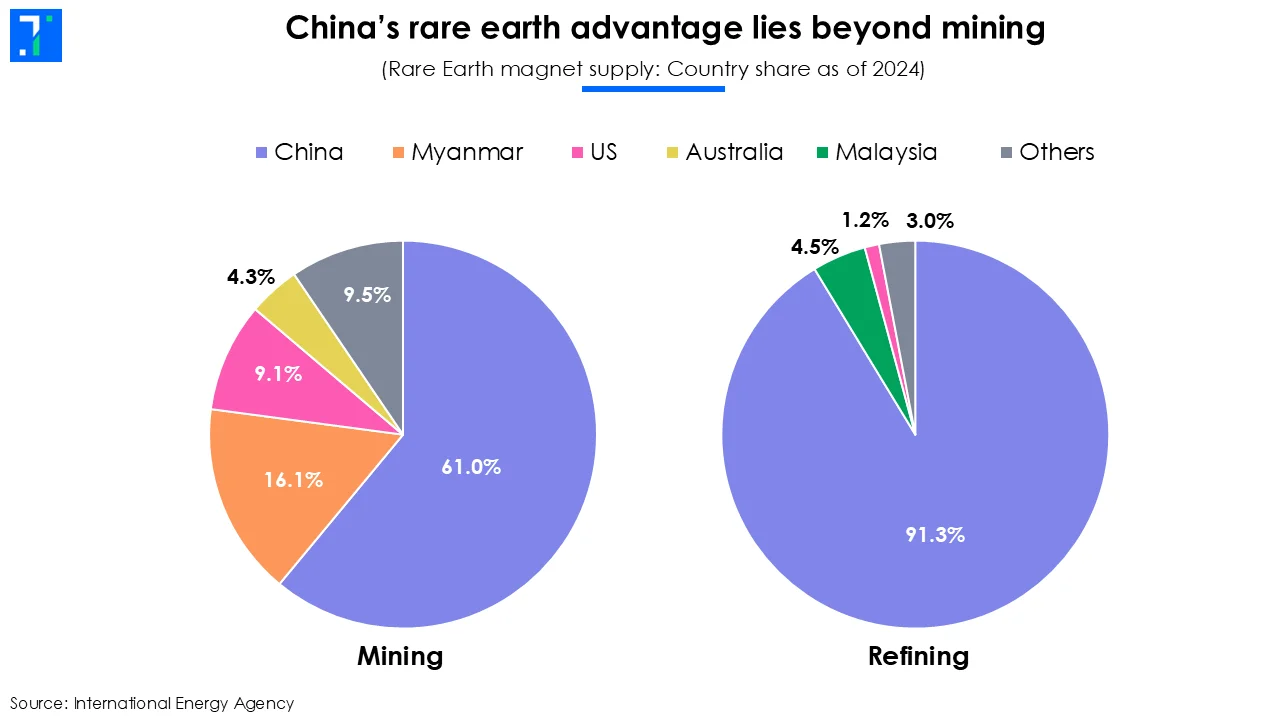

The inflection point came in late 2025, when China tightened export controls on rare-earth magnets and critical processing equipment. With China controlling roughly 90% of global rare-earth refining capacity, the move exposed a major vulnerability for Western manufacturers of electric vehicles, wind turbines, consumer electronics, and defense systems.

The US government has responded by signaling that it won't act just as a regulator, but as a strategic investor to secure access to critical materials. Just last month, the Trump administration took a 12% stake in USA Rare Earth for $1.6 billion, backing projects such as the Sierra Blanca mine in Texas and a magnet manufacturing facility in Oklahoma.

The Trump administration has already built stakes across the critical minerals supply chain, including rare-earth producer MP Materials, lithium developer Lithium Americas, and a Canadian base-metal miner, Trilogy Metals.

Processing capacity has become key as well. For years, ore extracted outside China still flowed back there for refinement, creating a hidden choke point. Companies such as Energy Fuels and Ucore Rare Metals are drawing attention by addressing this downstream gap by building processing and separation capacity in North America.

Gold makes a case to be in everyone’s portfolio

For much of the past two decades, US Treasuries anchored the global financial system, making up roughly 60–70% of global central-bank reserves in the early 2000s, while gold accounted for just 10–15%.

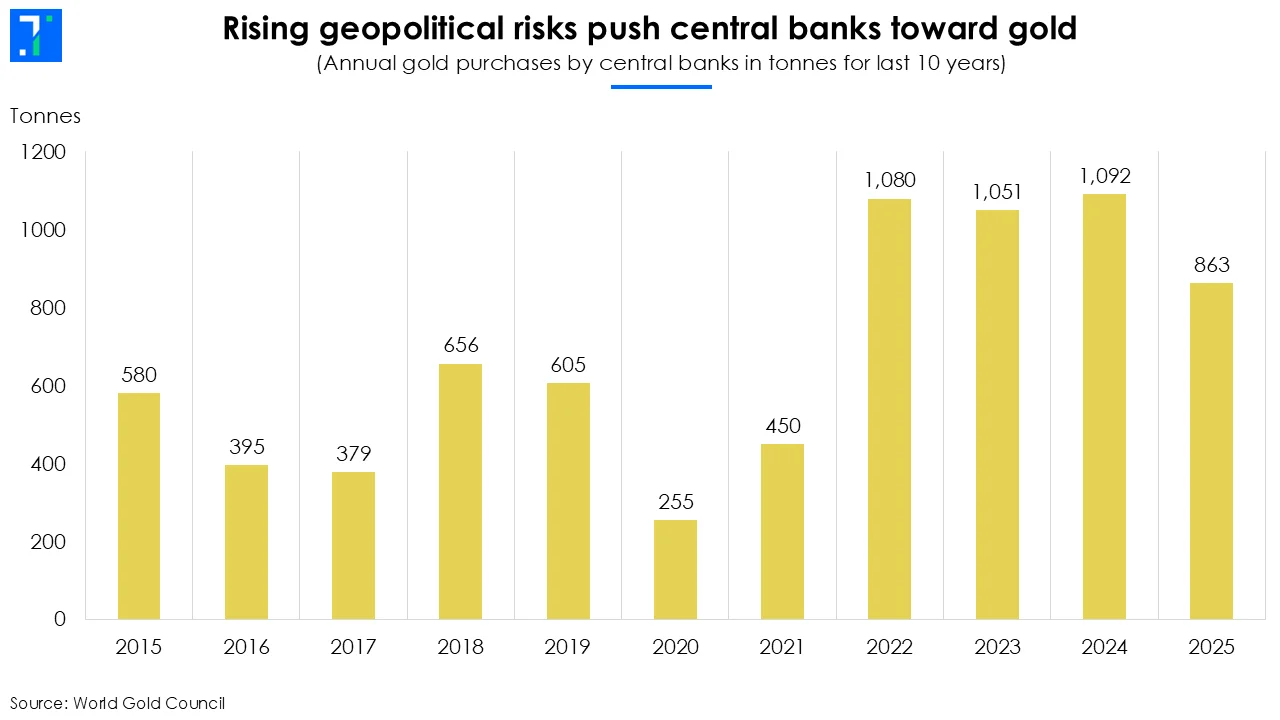

Trust in currencies can be risky, as countries change behaviour and priorities. The balance between the dollar and gold began to see-saw after the 2008 financial crisis, but the real break came in 2022, when Western governments froze Russian central-bank assets following the Ukraine invasion. The message to reserve managers was unambiguous: foreign-currency assets can become politically inaccessible. Since then, the reserve-management playbook has changed. High sovereign debt, repeated liquidity injections, and the expanded use of financial sanctions have made reserves more political.

Central banks have been buying accordingly. In 2025 alone, central banks purchased 863 tonnes, well above long-term averages.

Gold briefly sold off after Donald Trump nominated Kevin Warsh as Federal Reserve Chair, a move markets interpreted as signaling a more hawkish policy stance. The pullback prompted some tactical selling. George Efstathopoulos, a money manager at Fidelity International, said he reduced gold exposure ahead of what became the metal’s sharpest decline in decades.

He is now preparing to re-enter. “If we see another 5% to 7% correction, I’m buying,” Efstathopoulos said in an interview, adding that “a lot of the froth has been taken out, and the structural medium-term themes remain firmly in place.” Even after the pullback, gold remains up nearly 70% over the past year.

Precious metals mining companies such as Newmont, Barrick Gold, and Kinross Gold are benefiting from higher realized prices without proportional cost inflation. Industry executives argue the sector has finally broken the old “cost curse,” allowing price gains to flow more directly to margins.

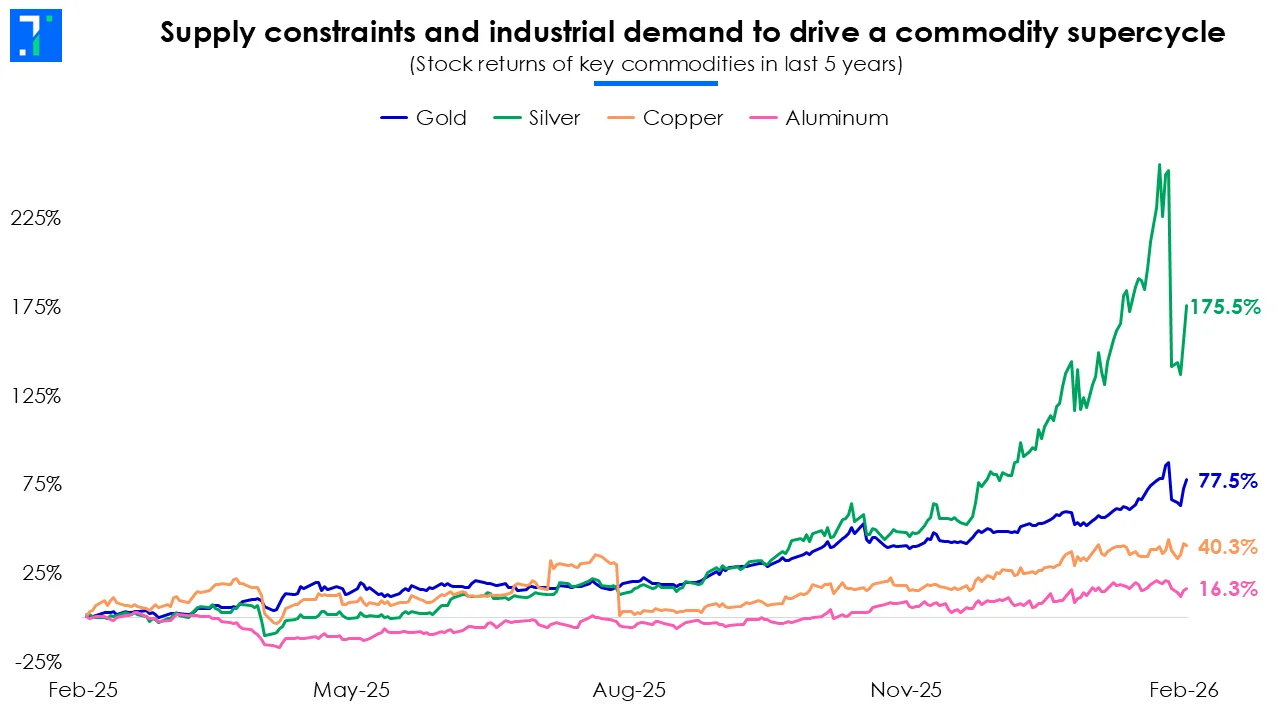

Base metals join the rally

The move extends well beyond gold and silver. Prices for copper, aluminum, nickel, and zinc rise alongside gold, reflecting what many traders describe as an “everything rally” in metals.

Unlike past cycles, this move is not driven by speculation alone, but is anchored in physical demand.

These metals sit at the core of electrification. AI data centers, power grids, electric vehicles, and renewable energy systems all require large quantities of copper and aluminum, while silver plays a critical role in advanced electronics. “Silver is the world’s best electrical conductor. High-speed connections in computers, smartphones, AI systems and data centers depend on it,” said Pan American Silver CEO Michael Steinmann.

Supply is struggling to respond. High energy costs and environmental regulations cap smelter output in China and Europe. Aging mines in Chile and Peru face declining ore grades, forcing miners to process far more rock to produce the same output as two decades ago.

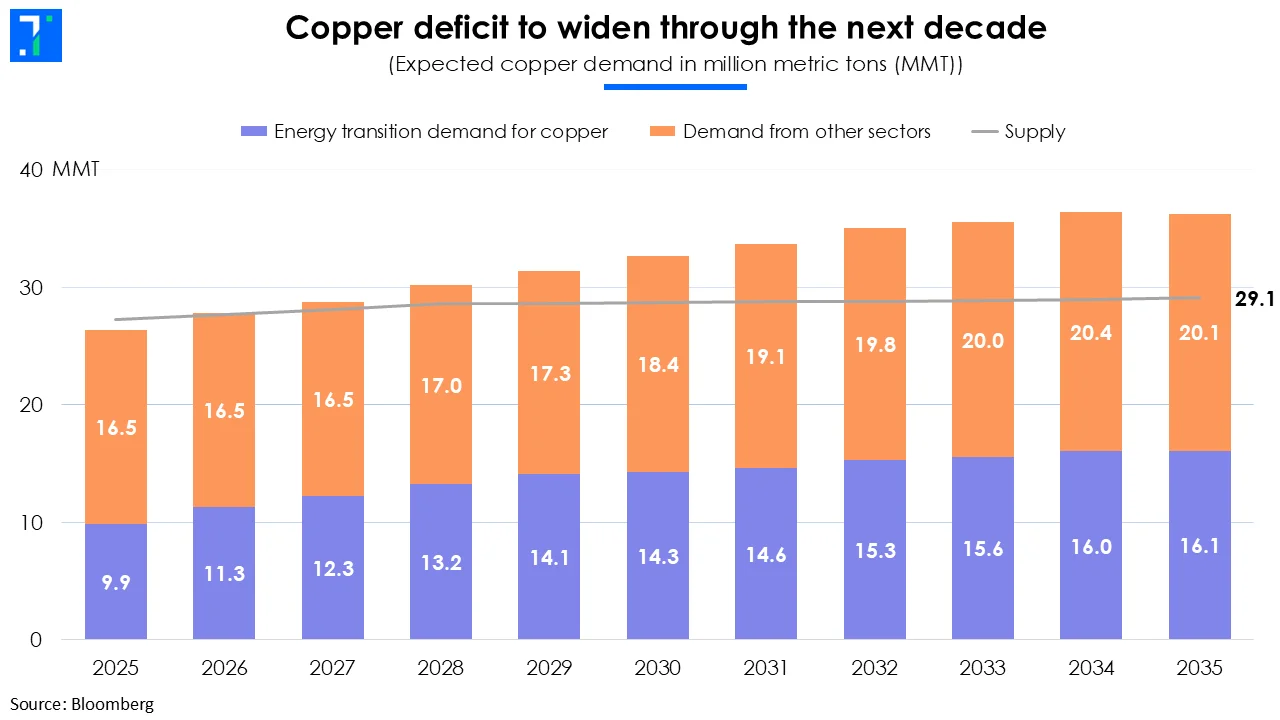

New supply takes time. A copper mine typically takes 15–20 years to reach production. Even at current prices, many greenfield projects fail to clear return thresholds. Most producers focus instead on incremental expansions at existing sites, and those additions remain limited.

Demand, meanwhile, keeps accelerating. Global electricity consumption is projected to rise by around 50% over the next decade, driving copper and silver use across power generation, transmission, and storage. The International Copper Study Group (ICSG) forecasts the refined copper market swinging to a deficit of 150,000 metric tons in 2026 from the previously expected surplus of 209,000 tons.

To satisfy this demand, Robert Friedland, Founder of a Canadian mining company, says, ”We have to mine the same amount of copper in the next 18 years as we mined in the last 10,000 years combined to maintain 3% GDP growth.”

Producers with scale stand to benefit most. Freeport-McMoRan and Southern Copper offer direct leverage to higher copper prices through long-life assets. In aluminum, Alcoa benefits from higher domestic pricing as tariffs raise import costs.

Taken together, these forces point to a fundamental revaluation of the mining sector. If this is a supercycle, it is not because commodities have become fashionable, but a shift forced by the world relearning an old truth: the digital economy still runs on physical resources, and those resources are finite.