“With President Donald Trump, volatility can rise rapidly and reverse just as quickly,” said Sagar Sambrani, a senior forex trader at Nomura. Trump, a man of unpredictable comments, unverified claims and seat of the pants decisions, is probably the most complicated head of state the markets have had to deal with.

That's not true for everyone, though. The stock market has seen sharp swings recently, and while many retail investors remain uncertain about the direction of markets, a small handful of participants seem to be trading with a crystal ball. Trading activity surged at unusual times, right ahead of Trump’s social media announcement of a five-day halt on strikes targeting Iranian energy sites.

A similar pattern is visible on Polymarket and other betting platforms, where large, concentrated bets are placed on geopolitical events just hours before they unfold. These include large bets on outcomes such as the capture of Nicolás Maduro and US-Israel strikes on Iran.

An on-chain analyst known as Andrew 10 GWEI highlighted a case of suspicious betting involving 38 accounts that he believes are controlled by a single entity, that made in total over $2 million by correctly predicting the February 28 strikes.

According to analysis shared on X, each account places four to ten bets with a near-100% success rate. The accounts began receiving cryptocurrency transfers on February 22, days before placing bets between 11:00 and 12:00 GMT on February 27, ahead of the anticipated strikes.

“All this points to insider activity,” Bubblemaps CEO Nick Vaiman said, pointing to the scale of profits, precise timing of trades, and the unusually high success rate.

In response, betting platforms tightened their rules, restricting trades based on non-public information and limiting participation by those who could influence outcomes.

As concerns grow, focus is shifting to whether the regulator is looking the other way.

The watchmen are leaving: exodus at the SEC

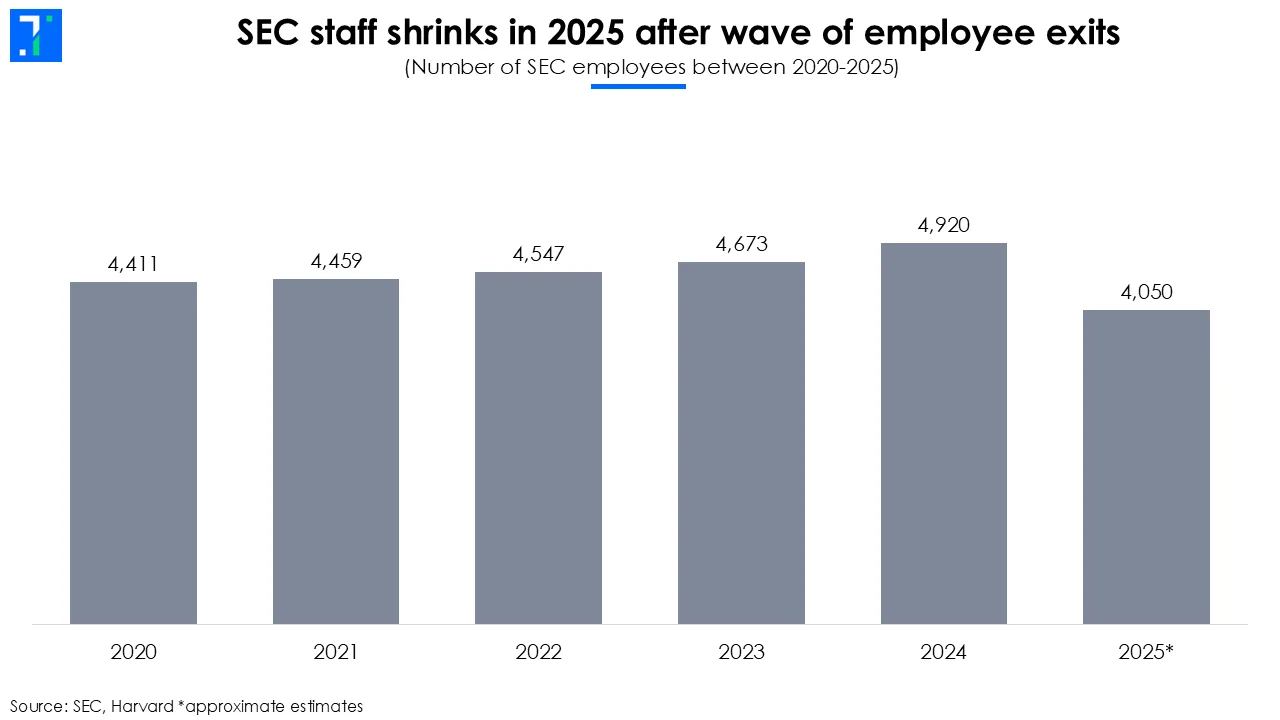

The US Securities and Exchange Commission (SEC) has been losing staff faster than the rest of the federal government. Exits have come in waves. Around 600 employees, about 12% of its workforce, left through buyouts by last May. By September, another 270 had departed outside these programs.

Together, this pushed the agency’s headcount down 18% in the 2025 fiscal year, pointing to a sustained thinning of staff.

Margaret “Meg” Ryan, the US SEC Director of the Division of Enforcement, resigned mid-March after just six months in the role. This high-profile exit has raised eyebrows across the financial industry. Ryan had reportedly clashed with agency leaders over the direction of the SEC’s enforcement program, including the 'unusual' handling of cases with ties to President Donald Trump and his family.

Weeks before her resignation, the SEC also settled rather than prosecuted a fraud case with Chinese crypto entrepreneur Justin Sun for $10 million. The case, filed in 2023, had accused him of unregistered sale of crypto assets and market manipulation that inflated TRX and BTT token prices by $31 million.

Sun is coincidentally, a major investor in a cryptocurrency project tied to President Trump. He holds $18.6 million in $TRUMP tokens, in addition to the $75 million he previously invested in World Liberty Financial, a crypto platform that directs 75% of revenues to Trump-owned entities.

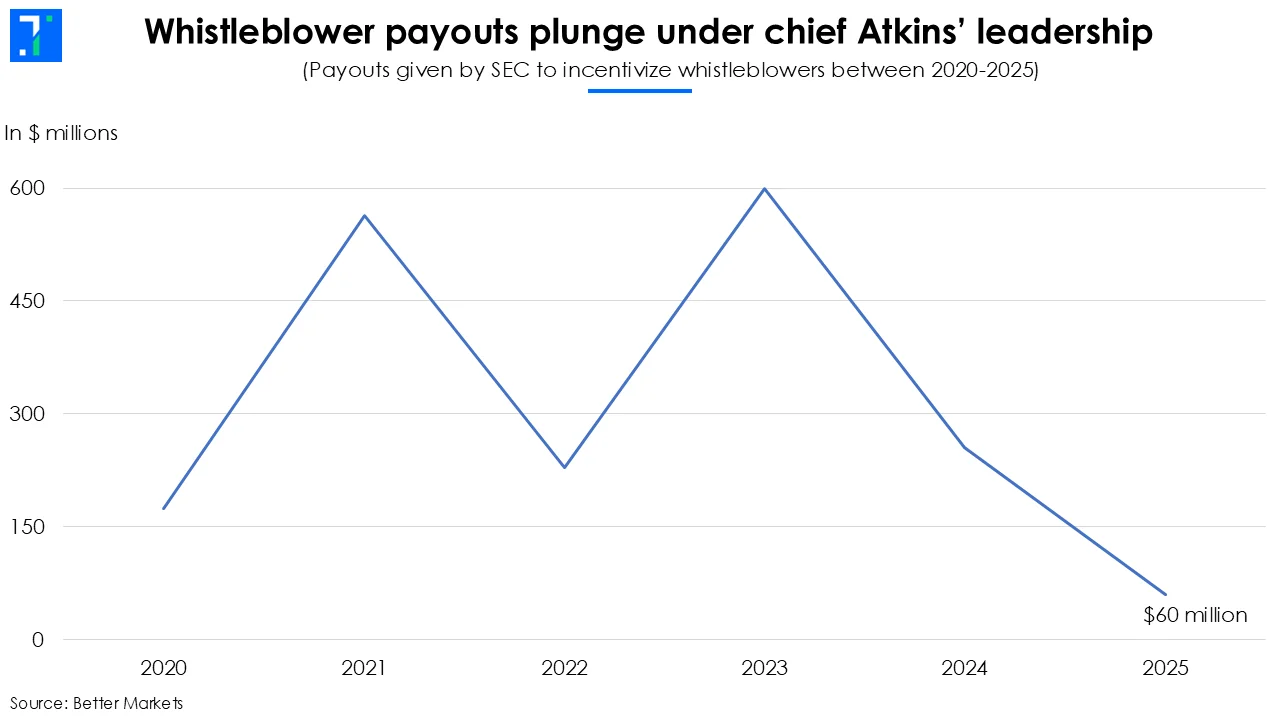

A key mechanism for uncovering insider activity is the SEC’s whistleblower program, which was designed to encourage individuals to report market misconduct by offering financial incentives. But recent data suggests a big decline. In FY25, the SEC awarded just over $60 million to 48 whistleblowers, a steep drop from $255 million in the previous year.

This drop reflects a shift in how claims are handled. The SEC rejected far more whistleblower applications, with hundreds turned down in final decisions. As a result, only 13% of cases led to payouts, down sharply from nearly 50% in 2022.

Stephen Kohn, a partner at a whistleblower advocacy firm, notes that the SEC appears to be applying stricter filters. “They are looking for hyper-technical reasons to disqualify someone,” he said, adding that this runs counter to the intent of the law, which was designed to encourage individuals to come forward and report misconduct despite the risks involved.

Fewer crackdowns, monetary settlements nosedive to a five-year low

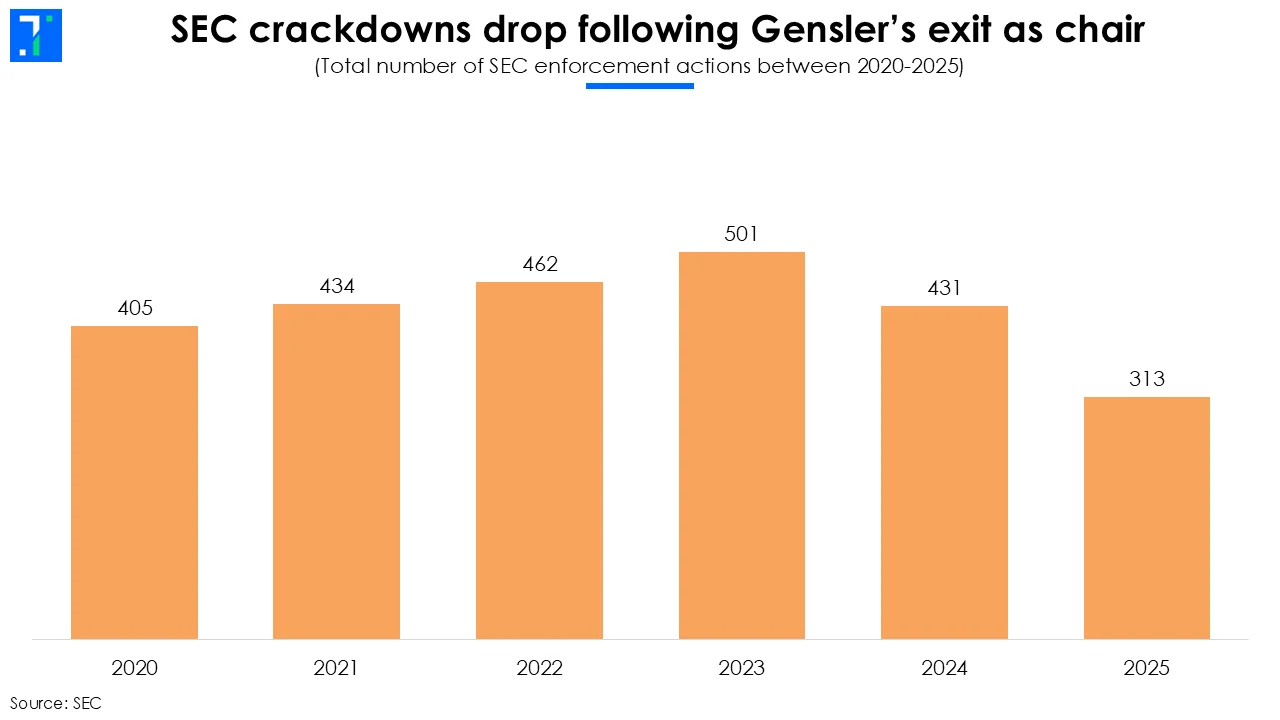

Even though the SEC has yet to release its official FY25 enforcement data, an analysis by Harvard Law School indicates that the agency brought 313 new enforcement actions, the lowest level in a decade. This marks a 38% drop from its recent peak in FY2023, where it recorded 501 new cases.

The slowdown is even more pronounced in actions involving public companies. The SEC recorded 56 such cases in FY25, down about 30% from the previous year. Of these, 52 were initiated under former Chair Gary Gensler, leaving just four actions under the new administration, marking the lowest annual count since 2013.

The shift also shows up in outcomes. Total monetary settlements fell 45% YoY to $808 million, the lowest since 2012 and well below the $1.9 billion average between 2016 and 2024.

Taken together, the data points to a clear slowdown in enforcement activity, both in the number of cases brought as well as the scale of penalties imposed.

From “Top Cop” to Facilitator

In his brief tenure, as chair Paul Atkins has called his taking over “a new day at the SEC”. The agency is moving closer to the Donald Trump administration’s push to position the US as a hub for digital assets.

Atkins has made it clear that he wants rules set upfront. The SEC’s Spring agenda included plans to simplify disclosure requirements and focus on what "truly matters" to investors. The aim, he said, is to rely less on after-the-fact action and more on clear guidance.

This shift is most visible in crypto. Within weeks of taking office, the SEC dropped its case against Coinbase, which had argued that some tokens were unregistered securities. Around the same time, it closed investigations into firms such as Gemini, Uniswap Labs, and OpenSea. Similar decisions followed through 2025 in cases involving Crypto.com, Binance, Robinhood, and Ondo Finance.

The change in approach is clear. The SEC is pulling back from earlier crackdowns while it reworks how crypto is regulated.

Even so, some major cases remain. The SEC is in settlement talks with Elon Musk over claims that he illegally delayed disclosing his initial stake in Twitter in 2022, which allowed him to buy more shares before the stake was disclosed.

A federal judge has allowed the case to proceed, with the agency seeking $150 million.

These cases show that while the broader stance is shifting, enforcement has not disappeared. But the trend is clear - fewer crackdowns, less manpower for oversight, and fewer whistleblower rewards.