Hi {firstname},

The recent panic unleashed in the stock market around AI, reflects two fears that are increasingly at odds.

One concern is that AI is set to disrupt entire segments of the economy so dramatically that investors are dumping the stocks of any company seen at the slightest risk of being displaced by the technology. Mentions of AI disruption in earnings calls surged to a record in Q4.

The other is a deep skepticism that the hundreds of billions of dollars that tech giants like Amazon, Meta, Microsoft and Alphabet are pouring into AI every year will deliver payoffs anytime soon.

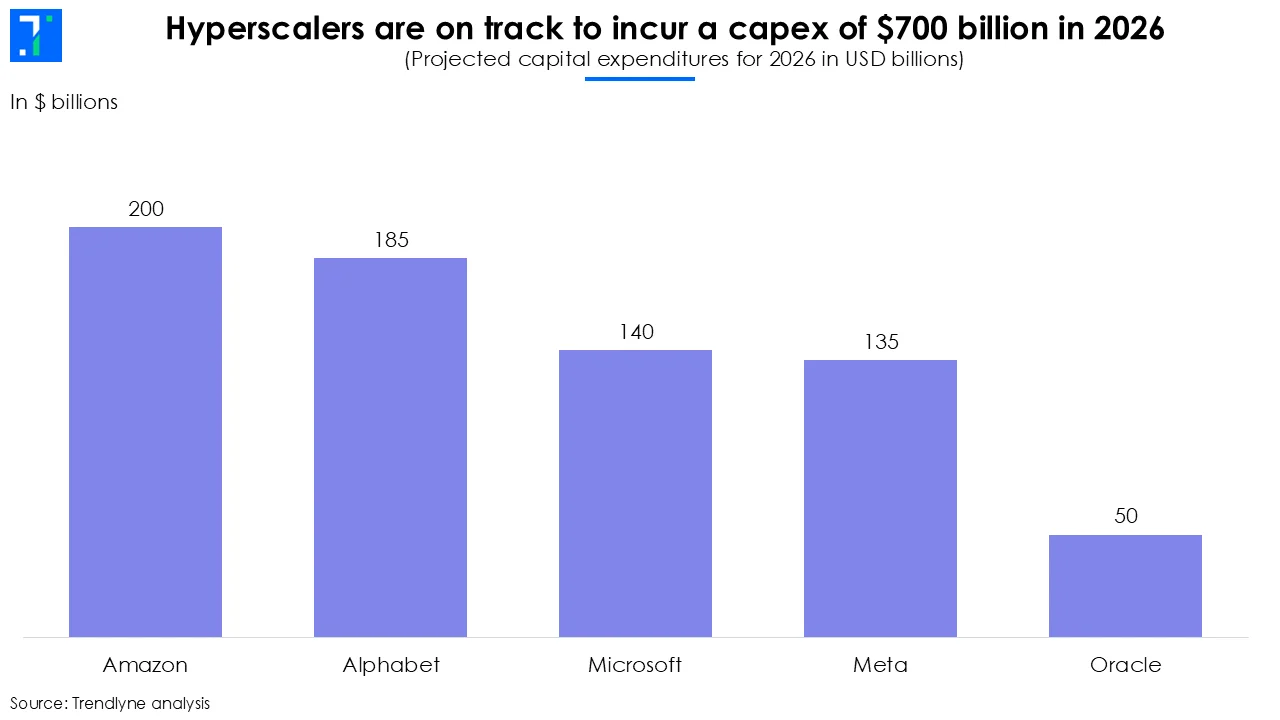

Take Amazon. The company recently outlined plans for $200 billion in capital expenditure for 2026, largely aimed at expanding its data center footprint to support AI workloads. Yet its cloud division, Amazon Web Services, has been growing at a slower pace than its peers.

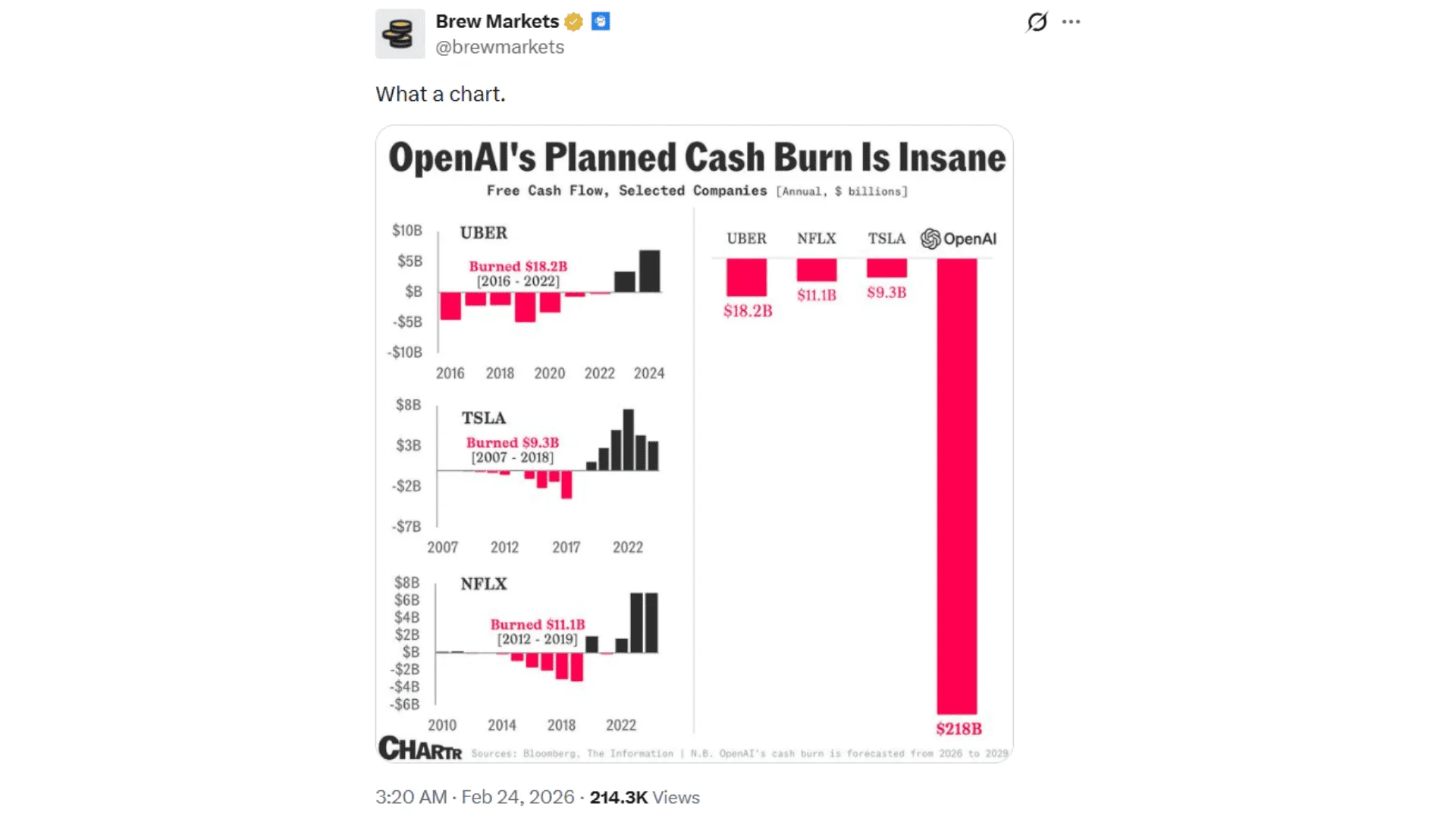

The scale of private sector spending is even more striking. OpenAI’s projected cash burn is unlike anything the notoriously high spending tech sector has ever seen before. The company expects to burn $218 billion between 2026 and 2029, about $111 billion more than the company’s internal projections from just two quarters ago. Even by Silicon Valley standards, the numbers are huge.

These dueling fears have been brewing for months, but became the focus of the stock market over the past few weeks. When markets try to price in two conflicting futures at once, volatility is the result.

In this week's newsletter, we assess where the market is headed.

AI models have improved a lot since their genesis

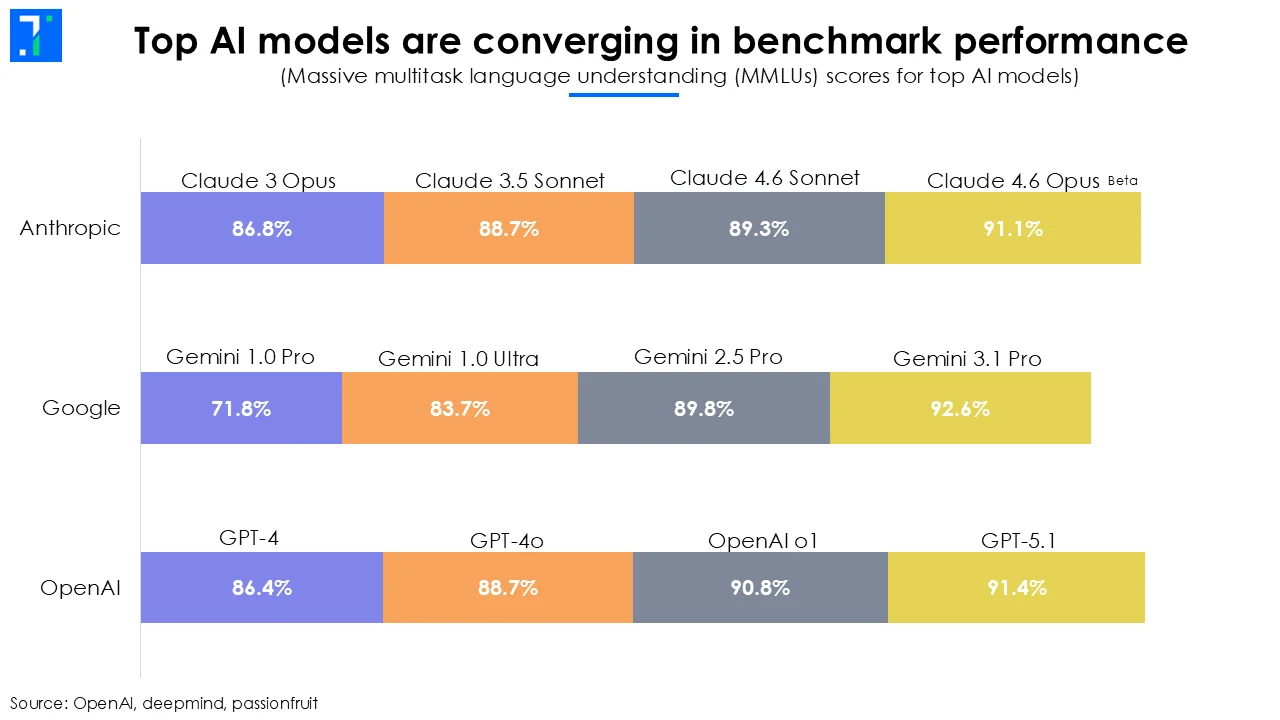

To see how much AI has improved, researchers use a benchmark called ‘massive multitask language understanding’, or MMLU. This is a lot like a comprehensive exam covering 57 subjects, including math, history, law and computer science.

The test measures whether a model actually understands tough questions across disciplines. It's the kind of exam not many humans, even the ones with tiger moms, can solve. Human domain experts on average score slightly below 90% in this test.

When GPT-3 was released in 2020, it scored about 44%. The model got many answers wrong. Recent models now score above 90%, which points to better accuracy and reasoning.

Models have also become more competitive with each other. Research by Moody’s notes, “AI models are converging in performance, making small differences in benchmark scores less important.” The study also finds that GenAI tools help professionals work faster while giving them access to more information and insights.

Most industry forecasts suggest that AI development is still in its early innings.

Consulting firms and technology strategists expect AI systems to become more autonomous, more specialized and increasingly embedded in enterprise workflows over the next three to five years. The focus is shifting from general chat interfaces to task-specific agents that can manage workflows end-to-end.

Hyperscalers ready to pour in trillions to advance AI

The scale of capital being deployed by the world’s largest technology companies is immense. The collective capital expenditure from the major AI hyperscalers is set to exceed $650 billion this year, 60% higher than in 2025, as they build out data center and AI infrastructure.

Players like Microsoft, Amazon, Alphabet, Meta Platforms and Oracle are expected to spend in aggregate about 90% of their operating cash flow on capex in 2026, according to Bank of America. That’s up from 65% in 2025.

The private side of the AI world is also fueling this build-out. OpenAI’s plans to spend up to $1.4 trillion on computing power over the next eight years, even as it continues to rack up heavy losses.

The cost of staying competitive in this space is clearly enormous, a Goliath versus Goliath matchup. Even companies generating tens of billions in revenue are burning capital at historic levels to maintain leadership.

OpenAI reached roughly $20 billion in annualized revenue by the end of 2025, yet it is projected to lose around $14 billion in 2026 as it continues investing heavily in new AI models. Anthropic, which owns Claude, shows the same gap. The company is valued at about 27 times revenue, while spending keeps rising. In 2026, it plans to spend about $12 billion to train models and another $7 billion to run them. The company now expects to turn cash-flow positive in 2028, one year later than its earlier projection. The valuation depends more on future outcomes than on current results.

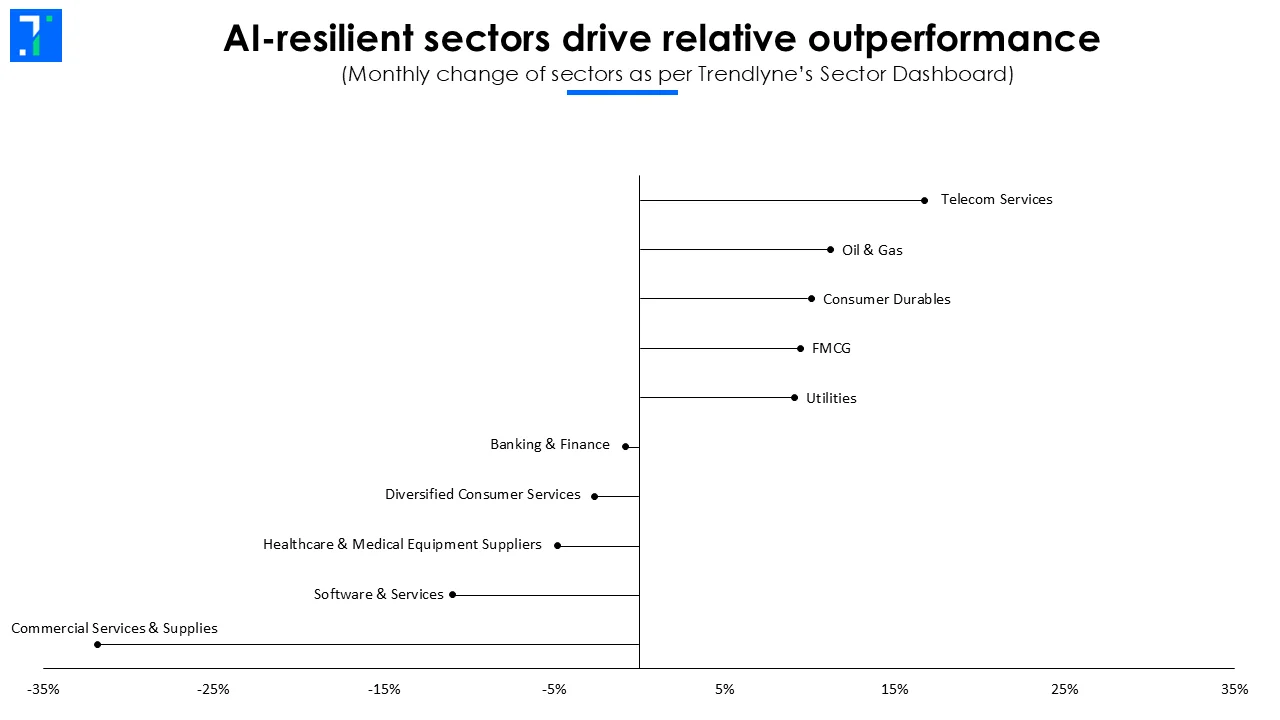

AI scare drives capital into bot-resilient sectors

On February 3, 2026, the S&P 500 Software Index fell 13% in a single session, erasing nearly a trillion dollars in market value.

If AI agents can perform tasks that once required teams of employees and multiple software subscriptions, demand for traditional software licenses could weaken. “We think application software faces an existential threat from AI,” said Nick Evans, a Polar Capital fund manager. His $12 billion global technology fund beat 99% of peers over one year and 97% over the past five.

After the sharp selloff, a growing group of investors is rotating toward sectors that appear less vulnerable to AI disruption. Instead of betting on who wins the AI race, they are asking: Which industries will continue to generate steady returns regardless of how the AI narrative plays out?

Trendlyne’s sector dashboard shows growing interest in Industrials, Energy, select Consumer Staples, and parts of Healthcare. These industries benefit from physical assets, regulatory complexity or human-centric demand that is harder to replace with code.

Importantly, these sectors are not completely AI-untouched, but are integrating it more selectively to raise efficiencies. Industrial firms are using AI for predictive maintenance, while Healthcare providers are applying AI for diagnostic support and administration. Energy companies are optimizing logistics and drilling efficiency through data-driven models.

Not everyone believes software’s pain will last. Michael Toomey, managing director of equities trading at Jefferies, noted that 73% of software stocks are oversold and that “we're due for a vicious rally in software.”

In this market, there could be value for investors in focusing on the fundamentals: companies with steady cash flows, improving macro conditions, and disciplined AI integration likely offer a more predictable path in returns, than trying to bet on the next AI model breakthrough.

As always,

The Trendlyne team